![]()

Advertiser Disclosure

Last update: November 17, 2024

6 minutes read

Student Loan Grace Period (Explained)

Learn about grace periods for student loans, managing repayments, and saving on interest.

By Brian Flaherty, B.A. Economics

Edited by Rachel Lauren, B.A. in Business and Political Economy

Learn more about our editorial standards

By Brian Flaherty, B.A. Economics

Edited by Rachel Lauren, B.A. in Business and Political Economy

Learn more about our editorial standards

Ever wondered what a grace period for student loans is and how it can affect you after college? It's a break between when you finish school and when you need to start repayments. You'll learn about the different grace periods for federal and private student loans, how interest accrues, and smart ways to manage your payments.

Key takeaways

- Grace periods for federal student loans typically last six months, with some exceptions

- Private student loan grace periods can vary and need to be discussed with the lender

- Interest on unsubsidized and private loans accrues during the grace period, and is capitalized afterward

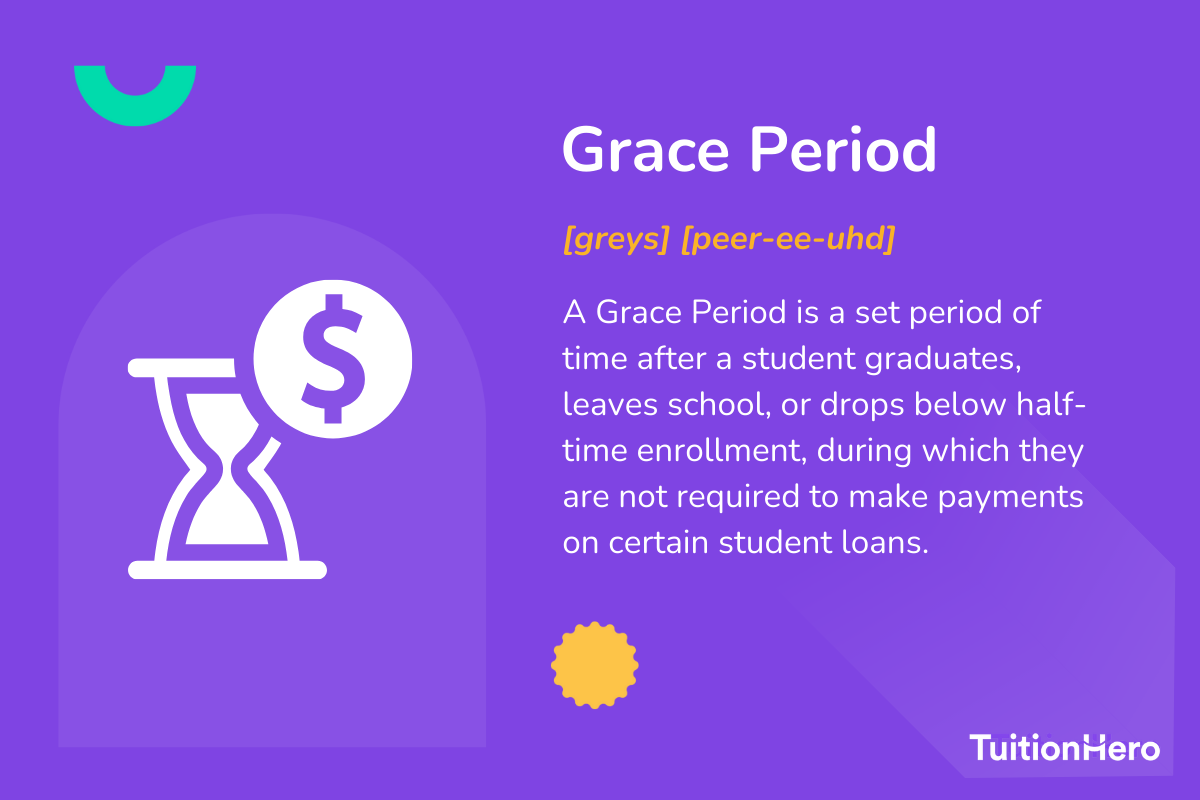

What is a grace period?

A grace period is a time after you finish school when you don't have to start paying back your student loans. With federal loans, this period is usually six months, but it can be different for private loans.

Bear in mind that it’s not just graduation that can trigger the start of your grace period. Depending on your loan terms, leaving school or dropping below half-time enrollment might also kickstart your grace period, meaning you’ll need to start repaying the loan after that time. Always double-check the terms of your student loan before making any major education decisions.

Do student loans have a grace period?

Yes, student loans usually come with a grace period. For federal student loans, the grace period is a standard six months, but it can hit up to nine months for specific loans like the Federal Perkins loan. Don't forget that private student loans are a different playing field—their grace periods can differ based on your lender's policy.

- Direct Loans: Six months

- Grad PLUS Loans: Automatic six-month deferment

- Parent PLUS Loans: Can request a six-month deferment

- Federal Perkins Loans: Nine months

When it comes to private student loans, it's crucial to check your loan agreement or reach out directly to the lender for the exact grace period details.

Do you pay interest during the grace period?

You don't have to make payments during the grace period, but interest might still add up. If you can, tackle the interest before your first payment to avoid it compounding on your principal balance.

- Subsidized Student Loans: No interest during grace period

- Unsubsidized Federal Loans: Accruing interest, capitalization after grace

- Private Student Loans: Accruing interest, capitalization after grace

When I was just getting out of school, I saw my student loan grace period as a great time to relax without needing to worry about making payments. But looking back, I could have saved a lot of money by starting payments right away and avoiding the buildup of interest.

TuitionHero Tip

Remember, even though you don’t need to make payments during the grace period, it still might be a good idea.

How does interest work during the grace period?

Understanding how interest adds up during the grace period is critical for your finances. Let's dive deeper:

Subsidized federal loans

Who wants free money? Well, with these loans, the federal government takes care of the interest while you're in school and during the grace period. You start fresh after, only owing your initial loan amount—a big help for graduates.

Unsubsidized federal and private student loans

Now, these are a different story. Interest starts piling up from day one, whether you're sipping coffee in class or enjoying that six-month grace.

When the grace is up, this interest gets added to your balance, increasing your debt. Paying the interest as it accrues is a smart move, as it can greatly decrease the total amount you'll pay over the loan's life.

Repaying your student loan smartly

When it's time to buckle down and repay, here's how to handle business:

- Get the details: Months before your grace ends, get the scoop on your loan terms, payments, and due dates.

- Budget for success: Work out how these payments fit with your income and expenses.

- Autopay for the win: Set up automatic bill payments to avoid late fees and keep your credit score happy.

- Pay extra if you can: Paying down your principal quicker means less interest and saying goodbye to debt sooner.

- Plans B and C: Deferment and forbearance options can pause payments if you hit a rough patch, just keep an eye on accruing interest.

- Reach out when you're stuck: Before you miss a payment, talk with your lender. They might work out a better payment plan that works well with your income.

Consider student loan forgiveness, especially if you work in public service or teaching (you could be eligible for the PSLF program). It could help clear your debt after meeting certain requirements.

Following these tips to make repaying loans simpler and less stressful.The key: understand your grace period and get ready for what comes next. Whether it's federal or private, you can navigate this period by coming prepared.

Compare private student loans now

TuitionHero simplifies your student loan decision, with multiple top loans side-by-side.

Compare Rates

Dos and don'ts of student loan grace periods

Understanding the grace period for your student loans involves making smart choices and avoiding possible mistakes. Knowing what to do and what not to do can help you avoid money issues and put you in a good position as you start repaying your debt. Let's explore some of these things.

Do

Do review your loan agreement to understand the specifics of your grace period.

Do make interest payments during the grace period if you can, especially for unsubsidized and private loans.

Do budget for your upcoming student loan payments before the grace period ends.

Do explore repayment options, like income-driven plans, if you think paying regularly might be a challenge.

Don't

Don't assume all loans have the same grace period.

Don't neglect interest that accumulates during the grace period.

Don't wait until the last minute to plan for repayment.

Don't ignore communication from your lender.

Advantages and disadvantages of student loan grace periods

When you finish school or graduate, you often get a bit of time before you need to start repaying student loans. It sounds good, but there are things to consider. Let's look at the positives and negatives of this time to help you make smart money decisions.

- Gives you time to find a job and get settled after graduating.

- No rush to start making payments right away, so you can plan your budget.

- For unsubsidized loans, it can delay the accumulation of interest a bit longer.

- Lets you explore and choose a repayment plan without feeling rushed.

- Interest might keep adding up on certain types of loans, making the total amount you owe more.

- There's a chance of not fully understanding the loan terms, leading to money mistakes.

- For some people, it might lead to delaying planning for repayment, making them less prepared.

- It's a temporary time, and relying too much on it might make you feel too secure, forgetting that you'll have to handle the financial responsibility soon.

Why trust TuitionHero

At TuitionHero, we want to make handling your student finances simple. As you move from college to the workforce, we're here to help. We offer different services like private student loans, loan refinancing, help with scholarships, and support with filling out the FAFSA form.

Our goal is to help you manage your education costs well. If you're thinking about dealing with loan interest during your grace period or looking for strategies to repay your debt, our team is here to guide you towards financial stability and success.

Frequently asked questions (FAQ)

Grace periods can be different depending on what you're dealing with. For example, grace periods on credit cards and bills work differently than for student loans. It's important to know what kind of grace period applies in your specific situation.

A grace period is a set time given before repayments need to be made, and it usually has specific conditions mentioned in an agreement. On the flip side, an extension is when two parties agree to give more time, and it might not be a part of the original deal.

If you start paying back your student loans before the grace period ends, you won't lose any of the remaining grace period time. But waiting and using the full grace period can be a good idea, especially if you need some time to get your finances in order after you graduate.

You can combine your federal student loans while in the grace period, but doing so might mean you lose the rest of the grace period. Before deciding, it's a good idea to check out what it means to consolidate and the advantages it may have.

Final thoughts

Understanding the grace period for your student loans is crucial after finishing college. It's a big moment that shapes how you deal with debt in the future.

Be proactive, stay informed, and make smart money decisions to build a strong financial future. TuitionHero is here to help you at every step. If you need more support and advice, check out our FAFSA Assistance to get ahead.

Source

Author

Brian Flaherty

Brian is a graduate of the University of Virginia where he earned a B.A. in Economics. After graduation, Brian spent four years working at a wealth management firm advising high-net-worth investors and institutions. During his time there, he passed the rigorous Series 65 exam and rose to a high-level strategy position.

Editor

Rachel Lauren

Rachel Lauren is the co-founder and COO of Debbie, a tech startup that offers an app to help people pay off their credit card debt for good through rewards and behavioral psychology. She was previously a venture capital investor at BDMI, as well as an equity research analyst at Credit Suisse.

At TuitionHero, we're not just passionate about our work - we take immense pride in it. Our dedicated team of writers diligently follows strict editorial standards, ensuring that every piece of content we publish is accurate, current, and highly valuable. We don't just strive for quality; we aim for excellence.

Related posts

While you're at it, here are some other college finance-related blog posts you might be interested in.

6 minutes read

What Are Pre-Orientation Programs?

Ever wondered how to make the most of your college start? Discover how pre-orientation programs can ease your transition and set you up for success before classes even begin.

Learn More

5 minutes read

How to Build a Strong Resume for Internships

Wondering how to craft a compelling internship resume that grabs attention? Discover essential strategies to build a standout resume and secure your dream internship.

Learn More

8 minutes read

How to Get Your Student Loans Forgiven

Learn how to erase student loan debt with our top strategies for Public Service Loan Forgiveness, including employer tips and payment plans.

Learn More

Shop and compare student financing options - 100% free!

Always free, always fast

TuitionHero is 100% free to use. Here, you can instantly view and compare multiple top lenders side-by-side.

Won’t affect credit score

Don’t worry – checking your rates with TuitionHero never impacts your credit score!

Safe and secure

We take your information's security seriously. We apply industry best practices to ensure your data is safe.

Finished scrolling? Start saving & find your private student loan rate today